This is the funniest thing I've read in at least a week. (From ![[livejournal.com profile]](https://www.dreamwidth.org/img/external/lj-userinfo.gif) sabotabby via nihilistic_kid.)

sabotabby via nihilistic_kid.)

The usually apolitical Smart Bitches, Trashy Novels gets political, and accordingly: Bill Napoli.

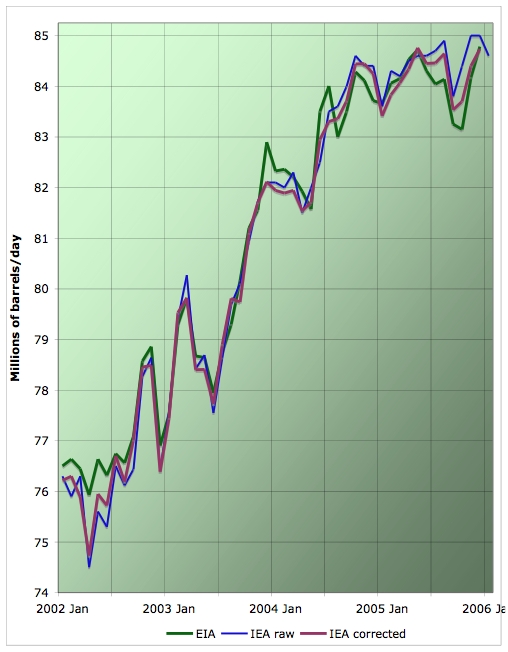

OPEC decides not to make its usual springtime production quota cut. They usually cut by one to two million barrels per day this time of year, because of rising and falling demand cycles. (Spring and fall are low demand; winter and summer are high. It's a good time to do maintenance, I'd imagine.)

We had an atypically warm winter this past year (despite the occasional zomg blizzard! moments), so month-to-month supplies are looking very good right now - in the US, a seven-year high for crude (same link as before), though refined product inventories have slipped a bit. Given that alone, you might typically expect OPEC to maintain their usual policy (link to a .jpg graph) of springtime production cuts, tho' maybe moderated a little bit. But they decided not to. The first answer as to why would be that this non-cut is to relieve price pressure and discourage exploration into alternates, along with some indication that, given prices right now, no cut would be respected. These are all valid motivators.

However, OPEC's primary concern for over a decade and a half - until around 2002 or 2003 or so - has been abject terror about another price collapse, as suffered in the late 1980s through the 1990s. The previous collapse harmed Arabic economies severely, and fears of a repeat have continued to dominate a lot of their thinking, so the fact that there wasn't even a token cut has real meaning. This failure to cut at all indicates that OPEC may no longer see price collapse as a significant concern. They apparently no longer see it as realistic in the short term at all - or, at least, no longer see it as an overriding concern, and given what their economies went through in the 1990s, the evidence for that has to be awfully, awfully strong. This, if true, is a major shift in perception of the markets on OPEC's part, with obvious ramifications for their understanding of supply and demand in upcoming years.

The usually apolitical Smart Bitches, Trashy Novels gets political, and accordingly: Bill Napoli.

OPEC decides not to make its usual springtime production quota cut. They usually cut by one to two million barrels per day this time of year, because of rising and falling demand cycles. (Spring and fall are low demand; winter and summer are high. It's a good time to do maintenance, I'd imagine.)

We had an atypically warm winter this past year (despite the occasional zomg blizzard! moments), so month-to-month supplies are looking very good right now - in the US, a seven-year high for crude (same link as before), though refined product inventories have slipped a bit. Given that alone, you might typically expect OPEC to maintain their usual policy (link to a .jpg graph) of springtime production cuts, tho' maybe moderated a little bit. But they decided not to. The first answer as to why would be that this non-cut is to relieve price pressure and discourage exploration into alternates, along with some indication that, given prices right now, no cut would be respected. These are all valid motivators.

However, OPEC's primary concern for over a decade and a half - until around 2002 or 2003 or so - has been abject terror about another price collapse, as suffered in the late 1980s through the 1990s. The previous collapse harmed Arabic economies severely, and fears of a repeat have continued to dominate a lot of their thinking, so the fact that there wasn't even a token cut has real meaning. This failure to cut at all indicates that OPEC may no longer see price collapse as a significant concern. They apparently no longer see it as realistic in the short term at all - or, at least, no longer see it as an overriding concern, and given what their economies went through in the 1990s, the evidence for that has to be awfully, awfully strong. This, if true, is a major shift in perception of the markets on OPEC's part, with obvious ramifications for their understanding of supply and demand in upcoming years.

{kind=link}